Trump Painted the Pool Blue. It Turned Green in Three Days.

The vanity project that explains why we stopped making things and started manufacturing the appearance of profit.

Donald Trump’s multimillion-dollar Reflecting Pool has been in the news lately for the embarrassing speed of its failure. Giant, city-block-sized algae blooms, among the largest in years, have swallowed the fresh paint job and made a mockery of the politicized rollout. It’s embarrassing. It also points at something deeper. This is a monument that demands continuous investment at a structural level to stay functional, and fixes that are purely cosmetic will fail. We’re watching that happen right now.

A metaphor, if you catch my drift. Happy Father’s Day, everyone. In the spirit of celebrating the people who made us, here’s what the pool keeps reflecting back. We’ve become a country that stopped making things and started manufacturing the appearance of profit instead. The rules that govern our financial markets are why, and they can be rewritten. A coat of blue paint over a leaking foundation is the whole economy in miniature, so let’s talk about how America makes, or doesn’t make, things anymore.

First, a little history. The Reflecting Pool was built in the early 1920s and has been renovated many times since to keep it working. It sits on the shifting, muddy flats of a former swamp on the banks of the Potomac. Like much of DC, it’s a monument to our ability to briefly and irrationally claim the riverbank for rectangular architecture. I’m all for that. One of the beautiful things about being human is our capacity to build sandcastles in the face of a rising tide. But it’s hard, expensive, and resource-intensive. It takes a constant structural fight against the moving base of land underneath to keep the water from leaking and the site from turning back into riverbank.

Before Trump, the most recent overhaul came under Barack Obama, a more than $30 million project finished by 2012 that drove new piles and rebuilt the structure to slow the leaking. Even that was understood to buy time, not stop the water forever. The land underneath doesn’t care about a ribbon cutting. The current administration now blames the Obama-era work for today’s mess, which tells you how it thinks.

Trump’s version came full circle, failing days after it went in. The $14 million no-bid contract went to a Virginia coatings firm, with a side cleanup deal handed to a company owned by a Trump donor and Mar-a-Lago neighbor. None of it touched the structure. It painted the bottom “American flag blue”, added bubblers, and installed filtration that couldn’t outrun three days of algae. A dark bottom collects more heat and makes conditions more favorable for algae, which the experts saw coming. He bragged about the color and how the pool stacked up against the tallest buildings in the world. He’s always been a shallow obsessive, interested only in the near-term presentation of success.

From making things to making profits

In a way, it’s exactly the renovation this American moment deserves, because it mirrors how we’ve come to think about making things over the past few decades. We’ve shifted from an economy that produces things to one that produces profits. Instead of building a structure that creates valuable goods, services, and real change in people’s lives, and letting prices and returns follow from that value, we’ve rearchitected the economy to manufacture the mirage of profit itself, without the underlying stuff.

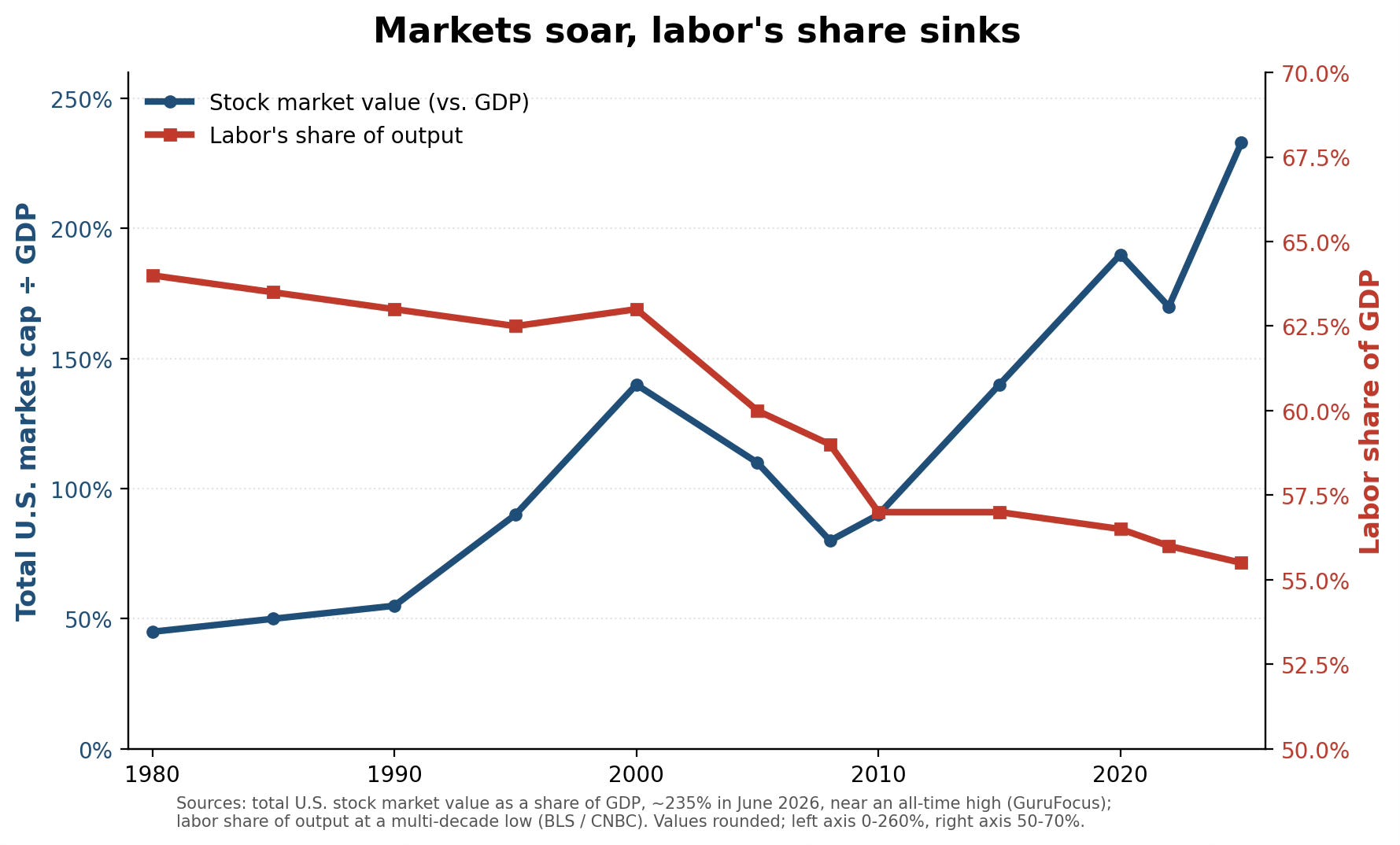

Take Elon Musk’s companies. Tesla trades north of 300 times earnings. SpaceX, which earns a tiny fraction of its valuation in annual revenue, went public in June at roughly $2.3 trillion and made Musk the world’s first trillionaire. It’s wider than those two. The total value of the U.S. stock market now runs near 235% of GDP, an all-time high, even as the country’s productive capacity grows slowly and, in places, stalls. And so the eerie feeling of a market soaring for years while real life feels sluggish and flat.

That gap is the whole story. Here it is in one picture: valuations have roughly quintupled against the economy since 1980 while labor’s slice keeps shrinking.

Step outside the market and the symptoms are everywhere. Employment runs high on paper but feels precarious. New launches outside software slow down. Housing production craters; the country is short nearly 4 million homes. We can’t build cars as cheaply as China, where the average electric vehicle now undersells a gas one and U.S. buyers face a $14,000 EV premium. We don’t make our own medicine; barely a quarter of the plants producing active ingredients for the U.S. drug supply sit on U.S. soil. We can’t release a phone anyone cares about. And the most advanced manufacturing, the cutting-edge chips that run everything, lives overseas, with Taiwan alone producing more than 90% of the world’s leading-edge semiconductors. It’s all the same story.

This is intentional. Our economy is doing what our markets were built to do, and much of it starts with the financial markets that steer resources in the first place. We used to assume those markets would automatically fund real businesses, which makes sense on its face. There’s no profit without selling goods and services people want. That’s where the money comes from.

For most of American history the relationship was simple. You put money into a venture, drilling for oil in the Southwest, panning for gold in California, building Model Ts, laying rail, smelting steel, and the goods sold because people valued them. These things cost a lot up front, so investors made possible what you couldn’t do alone. Dollars in, dollars out.

Over the past several decades, two things got much easier. First, trading on multiples of hypothetical future value. Second, harvesting value that was already there. They differ, but both consume value without creating it.

Betting on the future

The first you’ll recognize as the layered derivatives and sky-high valuations I mentioned, plus a fast-growing class of value built on the promise of future extraction: complicated IP schemes and speculative instruments like leveraged options. Katharina Pistor details these well in The Code of Capital, tracing how American law carves out abstract future value and sells it at a multiple to maximize the near-term return. The asset doesn’t have to do anything. It just has to promise.

And the engineering keeps stacking: derivatives on assets, then derivatives on those derivatives, then insurance on the whole tower, until the bets float almost free of whatever they’re supposedly about. The global pile of these contracts now carries a notional value around $846 trillion, more than seven times everything the world makes in a year. Before the 2008 crash, Wall Street spun up synthetic CDOs that held no mortgages at all and simply referenced other people’s mortgage bonds, so one bond could be wagered on by an endless number of side bets. In one case investigators later examined, $50 million in swaps rode on $12 million of actual mortgages (p.145 for the source).

Strip-mining the past

The second is extraction: the unregulated private equity and private capital that buys valuable assets, drains their current value while pretending it’s intact, then sells later at a markup. The clearest example is the sale-leaseback. An investment firm walks into a hospital or factory, sells the land out from under it, and leases it back at a monthly rate. That throws off millions in immediate profit without changing much month to month, since the property trades a mortgage for rent. But it wipes out decades of slowly built value. Steward Health Care sold its hospitals’ real estate for $1.25 billion, then drowned in inflated rent and collapsed into bankruptcy, closing hospitals that served low-income neighborhoods. A 2023 study found private-equity-owned hospitals saw a 25% jump in hospital-acquired complications even as they performed fewer procedures. Pair that with layoffs, longer hours, and degraded service, and you get a package worth materially less that can still post similar or higher monthly margins.

In both cases, we pay. We’ve just let pricing be defined by the people who profit from it rather than by the social value created. Sky-high valuations and the ever-expanding financialization of the economy have widened inequality into a K-shaped economy. The top 1% now hold nearly a third of all wealth, a concentration the World Inequality Lab says is close to its early-1900s peak, while labor’s share of output sits at a multi-decade low. Meanwhile, public companies sent shareholders a record $942 billion in buybacks in 2024, and CEO pay has climbed to 281 times that of a typical worker. On the other side, private capital has hollowed out the quality of nursing homes, healthcare, housing, dentistry, auto repair, and more, while still beating average returns.

The rotting belly

That feels impossible because it is. The relationship between financial markets and the real economy has been flipped. The system now produces, with ruthless efficiency, the plausible appearance of value while strip-mining the value it’s supposed to create. Brad Lipton at the Roosevelt Institute has a sharp piece on financialization’s harms that names many of them. We’ve flagged the pieces in isolation for years: the disdain for private equity, the Wall Street traders who crashed the economy in ’08, the investors buying up homes, the baffled anger at a billionaire class and a wealth gap that now rivals the Gilded Age and the run-up to the French Revolution. It’s also why countries like China are eating our lunch. Same problem.

Our financial laws, like the Securities Exchange Act, mostly assumed capital would find productive value on its own. So they aimed at fraud, deception, and disclosure, the right of people to get the information they need. But a century of very clever people making very clever tweaks has shown that with enough financial engineering, you can make money without making value.

This is the rotting belly of the American economy, and it’s the real existential threat we face against our rivals. It’s not just financial firms. Financialization has reset the incentives for every business: short-term profits, quarterly earnings, assets shifted overseas for tax treatment, revenue and workers moved wherever costs fall and booked value rises. That’s the actual secret behind China’s industrial edge. They invest, over five, ten, fifteen, twenty years, in the core structural capacity to produce value.

You can watch the logic run inside a single company. A manufacturer sitting on cash can build a new line, train workers, and chase a market that pays off in a decade, or it can buy back its own stock and lift the share price by Friday. Our rules reward the second choice and punish patience, so patience loses. Multiply that decision across the whole economy and you land where we are: record profits, hollow capacity, and a generation of managers who were never really asked to build anything that lasts.

Time to redraw the rails

Like our Reflecting Pool on its bed of mud, if we aren’t constantly reassessing and reinvesting in the structure, we’ll keep leaking the capacity that makes the economy work. Not for lack of trying. We’re a country full of hard workers and smart people, and the talent and the capital are both here. A coat of paint and a bubbler won’t fix it, and neither will one more disclosure rule or a single restriction on private equity.

So it’s time to reassess our relationship with the laws that move money around. We’ve spent the past few years talking about industrial policy, the government’s stewardship of funds and productive assets, from public factories to public investment, to actually make value. That matters, because the government, for all its own inane financial engineering, isn’t mainly in the business of profiting from illusion. But we also need a wholesale rethink of our securities, derivatives, and capital markets laws. Those laws set the bumper rails the economy runs between. Private credit, extractive buyouts, executive compensation, stock buybacks, indefensible price-to-earnings ratios, all of it is the norm because the system is calibrated to produce exactly that. The fixes aren’t mysterious. Tax stock buybacks like the income they are. Cap the debt a buyout can pile onto the company it buys. Bar sale-leasebacks on hospitals and other infrastructure people can’t live without. Make patient, long-term investment cheaper to choose than a quick pop in the share price. None of it is radical on its own, and that’s the point. We can take the reforms one by one, but we need to start treating this as a single story about making our financial economy deliver value again. Otherwise we’ll be stuck playing whack-a-mole against very clever people with very expensive lawyers, paid for by new debt loaded onto your grandma’s nursing home with an arcane new derivative.